Our trading specialists carry out a periodic analysis of the European electricity market for the utilities we accompany as technology partner. You can now have access to one of the most recent and relevant studies.

The course of the Iberian electricity market during 2022 was conditioned by multiple circumstances: both the mechanism to adjust production costs (the so-called “Iberian exception”) and the worldwide economic context, which is influenced by inflation, added up to the continuous integration of renewable energies in the generation mix and the energy contingency resulting from the current geopolitical situation. In addition, the COVID maintained part of the protagonism that it gained during the previous years.

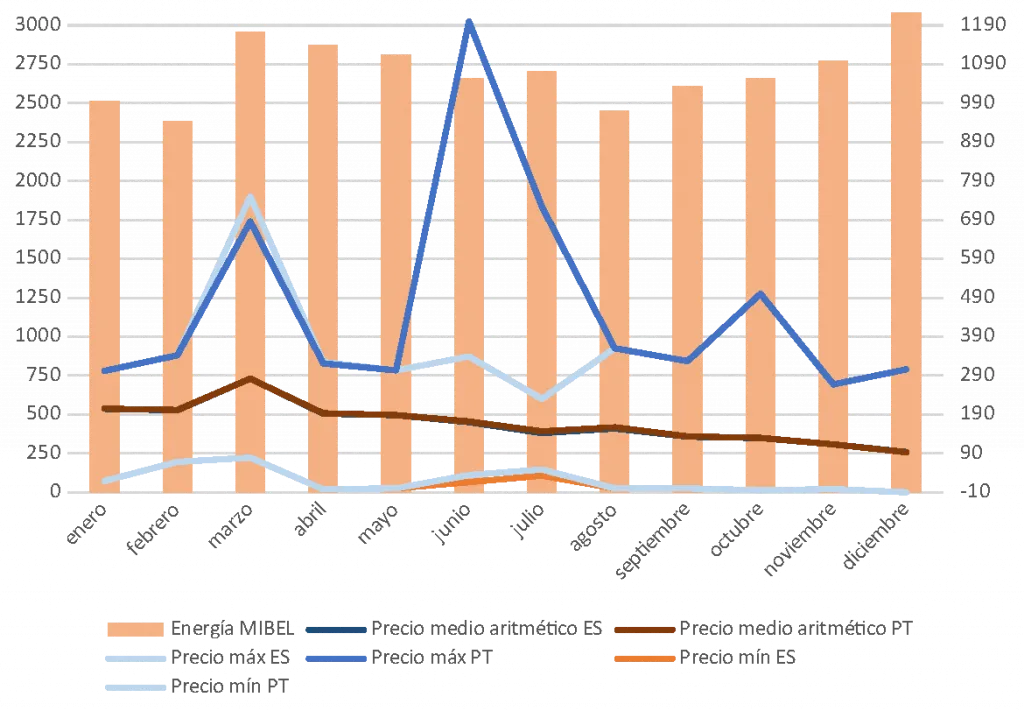

Below, we will present an analysis of the evolution of the Iberian electricity market –focusing especially on the Spanish zone– within the framework described above for 2022 compared to the previous year.

Record economic volume despite the decrease of the negotiated energy

Regarding the economic volume, 2022 marked an all-time high in negotiated purchases in the day-ahead and intraday markets: €51,149 million (69.2% higher than in 2021); €41,164 million in the Spanish zone and €9,985 million in the Portuguese zone. It is important to stress that this achievement was due to the rise in the market’s prices, despite the fall of the total amount of exchanged energy, which was 257.8 TWh (3.4% lower than in 2021).

The final average annual price of the Spanish electricity system’s demand in 2022 was 204.50 €/MWh, which is a record (+72.3%) despite the decrease in the national demand in busbars, 235,459 GWh (-2.9%).

The impact on the holders of units of the cost of the adjustment mechanism was of €6,663 million (included in the aforementioned €51,149 million of total economic volume), with an average value of 72.93 €/MWh.

Although almost the entirety of the Spanish electricity generation came from renewable and nuclear energy –and that coal-fired power plants only contributed 2.8% to the generation mix–, combined cycle went up by 227.2% and contributed 18.4% of the generation. In the Portuguese zone the values were similar, although with more limited decreases in general, with a noteworthy 0% coal contribution.

Day-ahead market

The day-ahead market remained as the main MIBEL market: from the total 257.8 TWh negotiated in 2022 in the markets where OMIE operated, 226.8 TWh belonged to the DAM. This data represented a 1.6% less than in 2021, 174.7 TWh (-1%) corresponding to Spain and 52.1 TWh (-3.3%) to Portugal.

In contrast to the negotiated energy, the prices increased in an extraordinary way: the average price of the day-ahead market of the MIBEL was 167.72 €/MWh, which resulted in a growth of 49.8% compared to 2021. If we take the national markets into consideration, this price was 167.53 €/MWh in Spain (+49.7%) and 167.9 €/MWh in Portugal (+49.9%).

The main technologies considered when marking the marginal price were hydraulic, combined cycle and the biomass-cogeneration-waste group, with respectively 37.8%, 29.4% and 13.2%.

It is worth noting that, on May 10th 2022, the maximum price limit of offer for all the zones participating in SDAC was established at 4,000 €/MWh. On June 15th, the adjustment mechanism came into force, and its impact on the market is still under discussion today.

Intraday auction market

In the intraday auction market, the average price was 167.21 €/MWh, 0.3% lower than the DAM.

2022 was crucial for the roadmap and the design of new IDAs, which will be implemented in 2024.

Intraday continuous market

The intraday continuous market, which had a stable negotiation trend throughout the year, reached a peak of 782.4 GWh negotiated in April last year. The average price was raised to 174.92 €/MWh, 4.3% higher than that of the DAM [Click on the banner below to read more]